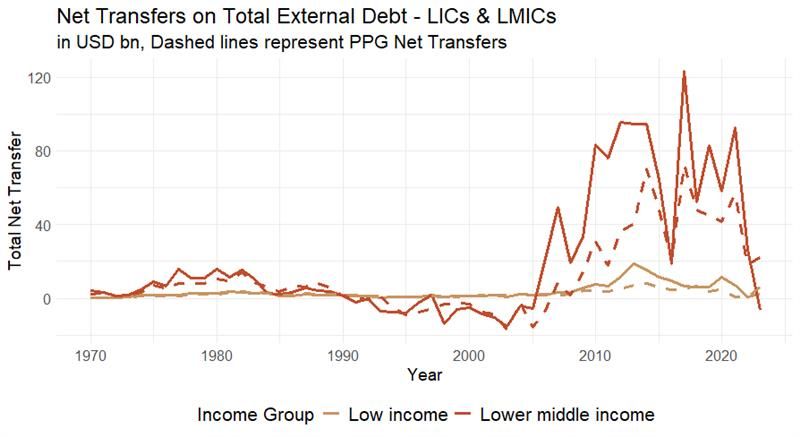

In 2023, the global financial system witnessed a striking reversal. For the first time in over a decade, lower- and middle-income countries (LMICs) experienced negative net financial flows on external debt, amounting to -$7 billion. The reversal of financial flows from lower- and middle-income countries (LMICs) to developed countries, is a moment of reckoning for global development finance.

(Source image: Finance For Development Lab, 2025)

While net positive financial flows from the Global North to the Global South have historically been framed as evidence of solidarity and non-exploitation, this reversal exposes a troubling asymmetry: LMICs are now directly subsidising wealthier nations, depleting their reserves and undermining their development trajectories. This outflow highlights a troubling reality: the global financial architecture is failing the very countries it claims to support.

The prevailing response to development finance challenges has been a pivot toward financialization, epitomized by the Wall Street Consensus. This paradigm positions multilateral development banks (MDBs) as pivotal actors tasked with mobilizing private capital to fill financing gaps for sustainable development and climate goals. Yet, this approach has led to a misplaced optimism about the transformative potential of private finance. The results, as recent trends illustrate, have fallen dramatically short of expectations.

A Financialized Approach: Promises and Pitfalls

The financialization of development finance is rooted in the notion that leveraging public resources to attract private capital can unlock the trillions needed to achieve global goals, such as the climate transition and sustainable development goals. The European Union is no stranger to this approach; its 2021 reform of the EU financial architecture for development through instruments such as NDICI-Global Europe, illustrates its alignment with this belief in private finance as a central pillar of development (Bougrea et al, 2022). MDBs, central to this strategy, have been reoriented toward “de-risking” private investments through mechanisms such as blended finance and securitization. These efforts, however, reveal fundamental limitations.

While MDBs are increasingly encouraged to adopt market-oriented practices, their institutional frameworks—grounded in sovereign lending and preferred creditor status—are at odds with the demands of large-scale private capital mobilization. This tension results in what can be termed a trilemma: MDBs must balance maximizing external investment flows, derisking private finance, and preserving their traditional lending models (Bougrea & Vermeiren, under review). The dominance of “project derisking” over “portfolio derisking” reflects an institutional conservatism that prioritizes internal stability over transformational change, but at the cost of scalability and impact.

The Structural Failure of Financialization

Critiques of the Wall Street Consensus have rightly pointed to its inability to address the systemic challenges facing LMICs. Private capital remains inherently pro-cyclical, prioritizing high returns and risk aversion over long-term development impact. This financial volatility exacerbates the inequalities it purports to alleviate, leaving LMICs vulnerable to external shocks and perpetuating cycles of indebtedness.

The focus on financialization also obscures deeper issues within the global financial architecture. The reversal of financial flows is symptomatic of a broader extractive dynamic, where LMICs bear the burden of high debt servicing costs, restrictive lending terms, and an overreliance on market-based solutions. This model not only fails to meet development needs but actively undermines the fiscal autonomy of borrowing nations.

How to: A More Equitable Financial Architecture?

The reversal of financial flows calls for a fundamental reimagining of the global financial system. This requires moving beyond incremental reforms and addressing the structural asymmetries that have entrenched inequality between the Global North and South.

- Reinforcing Sovereign Lending: MDBs must prioritize their traditional strengths, particularly countercyclical lending and support for public investment in infrastructure, education, and health. In other words: non-bankable sectors. By strengthening these pillars, MDBs can refocus on long-term development outcomes rather than short-term financial gains.

- Restructuring Governance: The governance of MDBs reflects the disproportionate influence of wealthier shareholders, often to the detriment of borrowing nations. Expanding the voice and representation of the Global South in MDB decision-making processes is essential to ensure that development finance aligns with the needs of recipient countries.

- Rethinking the Role of Private Capital: While private finance will continue to play a role in development, it cannot be the cornerstone of the system. Alternatives such as regional development banks, South-South cooperation, and enhanced public financing mechanisms must be elevated to reduce dependence on market-based solutions.

- Addressing Resource Flows: Reversing the outflow of financial resources from LMICs requires a multifaceted approach, including debt relief initiatives, increased concessional financing, and mechanisms to enhance fiscal autonomy.

The Path Forward

This moment presents an opportunity to critically assess the failures of the existing financial architecture and reorient its priorities. The continued reliance on financialization as a panacea for development challenges reflects an entrenched belief in the neutrality of markets—a belief that this crisis has decisively undermined.

Reforming the global financial system is not simply a technical exercise but a profoundly political one. It demands that we confront the power dynamics that have long shaped international development finance and imagine a system that prioritizes equity, sustainability, and resilience over the interests of the few.

The question, then, is not whether reform is needed, but whether the political will exists to make it happen.

Leave a comment